Last year saw many taxpayers selling appreciated assets. The primary reason for this activity was the imminent increase, in 2013, of the long term capital gain rate, and the imposition (in some cases) of a 3.8% tax on net investment income, both of which would impact sales of assets owned directly by individuals or by pass-through entities owned by such individuals, including S corporations.

Notwithstanding the foregoing tax rate increases, 2013 may be a good time for certain S corporations to consider a sale of assets.  Built-in Gain Tax

Built-in Gain Tax

Unlike C corporations, S corporations generally pay no corporate-level tax. Instead, items of income and loss of an S corporation pass through to its shareholders. Each shareholder takes into account its share of these items on its individual income tax return. Thus, any gain recognized by an S corporation on the sale of assets is passed through and taxed to its shareholders.

There is an exception to this rule for asset sales by S corporations that were previously taxed as C corporations. Specifically, under Section 1374 of the Internal Revenue Code (the “Code”), a corporation level tax, at the highest marginal rate applicable to corporations (currently 35%), is imposed on that portion of an S corporation’s gain that arose prior to the conversion of the C corporation to an S corporation (the “built-in gain” inherent in its assets at that time; “BIG”) and that is recognized by the S corporation during a specified period of time following the conversion (the “recognition period”).

The amount of corporate BIG tax imposed upon the S corporation is treated as a loss taken into account by the corporation’s shareholders in computing their individual income tax. The character of the loss is based upon the character of the BIG giving rise to the tax; thus, the sale of an asset that produces a capital gain would generate a capital loss.

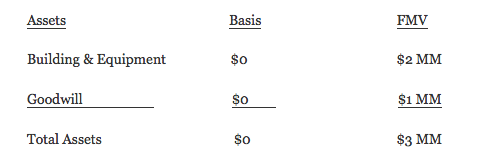

Assume, for example, that ACME Inc. was a C corporation with no liabilities and with the following assets on January 1, 2010:

ACME made an S election effective January 1, 2010. The BIG inherent in its assets is $3MM. In 2013, ACME sells its assets to an unrelated third party for $3.5 MM. The sale occurs within ACME’s recognition period. Of the $3.5 MM gain recognized, $3 MM represents BIG and is subject to corporate level tax at a 35% rate. Thus, ACME is liable for $1.05 MM of corporate income tax. Because ACME is an S corporation, the gain recognized passes through to its shareholders, who are also allocated a loss in the amount of the tax liability arising from the BIG. Thus, the shareholders are allocated $3.5 MM of gain and $1.05 MM of loss, they pay a 20% capital gain tax, and they net proceeds of $1.96 MM: sale proceeds ($3.5 MM) minus corporate tax ($1.05 MM) minus individual capital gains tax ($490K).

By comparison, if the asset sale had not been subject to the BIG tax, there would have been no corporate tax, the $3.5 MM of gain recognized by the corporation would have been taxed only to the shareholders (at 20%), and they would have retained $2.8 MM of the sale proceeds.

Recognition Period & ATRA

Given the economic impact of the BIG tax, shareholders have historically been reluctant to cause their S corporation to sell its assets during its recognition period.

Before 2009, this period was defined as the first ten taxable years that the S election was in effect. However, Congress temporarily reduced the recognition period to five tax years, and the American Taxpayer Relief Act of 2012 (P.L. 112-240; “ATRA”) extended the five-year period to include tax years beginning in 2013. Thus, with respect to any pre-conversion BIG, (for sales occurring in 2013) no tax will be imposed under Section 1374 if such sales occur after the fifth taxable year the S corporation election is in effect.

2013

In light of the foregoing, 2013 may be a good time for an S corporation that converted from C corporation status in 2007 or earlier to consider selling all or some of its assets.

As an illustration, assume ACME Inc. was a C corporation that elected to be taxed as an S corporation beginning on January 1, 2008. At that time, it had net unrealized BIG of $3 million. Prior to ATRA, if ACME had sold its assets in 2013 and recognized gain of at least $3 million, then the entire BIG would have been subject to corporate level federal income tax because the sale would have occurred within the ten-year recognition period.

Under ATRA, however, the recognition period is reduced to five years. Since ACME will have been an S corporation for five years at the end of 2012, its recognition period will end at that time, and any gain on the sale of its assets in 2013 will escape corporate level taxation, even if that gain is recognized and taxed after 2013 (during what would have been the 10-year recognition period before ATRA) under the installment method.

Notably, the ATRA provision that reduced the recognition period to 5 years expires at the end of 2013, and the ten-year recognition period is then reinstated. Thus, if ACME delays the sale of its assets to any time from 2014 through 2017, it will be subject to corporate tax on its BIG.

Conclusion

The foregoing is not to suggest that a pre-2008 S corporation with assets subject to the BIG tax should hurry to sell those assets only to capture the tax benefit afforded by ATRA before it expires. However, an S corporation that was otherwise contemplating a sale should consider the fact that the shortened recognition period expires at the end of 2013, thereby increasing the tax cost of a later sale.

This article originally appeared in the May 2013 of The Suffolk Lawyer.